Harvia Stock Jumps 15% on Record Q1 Revenue of EUR 58.6M

All four regions grew. North America added 21% in local currency. But the real variable is a factory IT cutover in Muurame that will shift EUR 3-5M from Q2 into Q3.

Harvia Q1 2026 interim report: record revenue with strong profitability. Source: Harvia Plc.

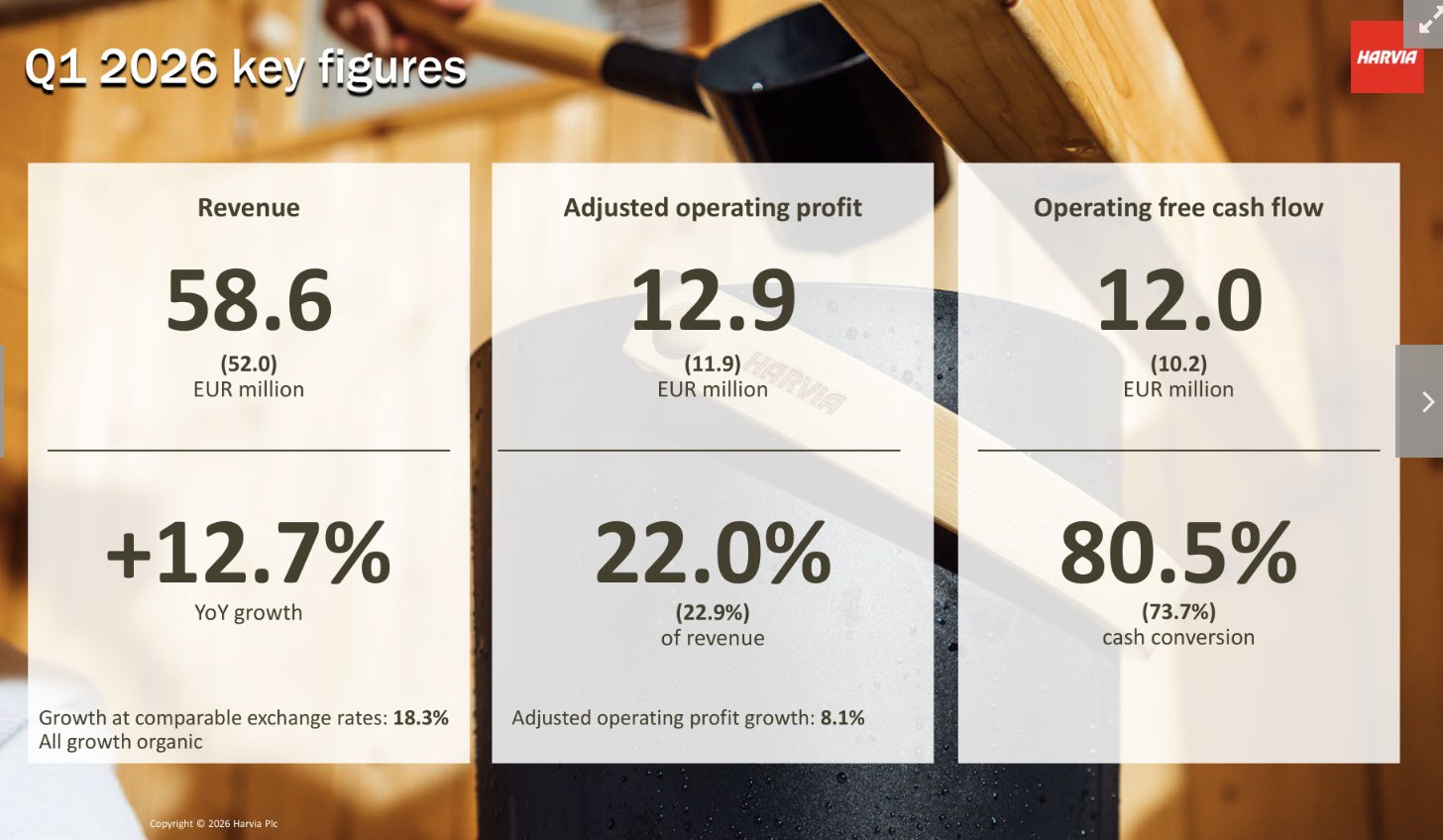

Harvia shares surged nearly 15% on the Helsinki exchange on May 7 after the Finnish sauna manufacturer reported its highest-ever quarterly revenue: EUR 58.6 million in Q1 2026, up 12.7% year-over-year. At comparable exchange rates, the growth was 18.3%. Earnings per share rose 11.9% to EUR 0.50.

Three of four regions delivered double-digit gains. Every euro of growth was organic. The stock closed at EUR 41.05, up 14.7%, then gave back 6.1% to EUR 38.55 on May 8. It was Harvia's second-largest single-session move of the preceding year, behind the 22.5% jump on the Q3 report in November.

The headline numbers were clean. But beneath them sits an operational variable that will shape how the next two quarters read: a major IT and process overhaul at Harvia's headquarters and production facility in Muurame, Finland, that management expects to shift EUR 3 to 5 million in deliveries and related gross margin from Q2 into Q3.

Key Facts

- Q1 2026 revenue: EUR 58.6M (+12.7% reported, +18.3% at comparable exchange rates)

- Adjusted EBIT margin: 22.0% reported (22.4% at comparable FX)

- EPS: EUR 0.50 (+11.9% year-over-year)

- North America: EUR 24.4M (+12.0% reported, +21.1% in local currencies)

- APAC and MEA: +29.7%, fastest-growing region

- Northern Europe: +16.7%, third consecutive quarter of double-digit growth

- Operating free cash flow: EUR 12.0M (cash conversion 80.5%)

- Net debt: EUR 49.4M (1.0x net debt-to-EBITDA vs. 2.5x target ceiling)

- Employees: 761 (up from 728 a year earlier)

- Muurame IT shift: EUR 3-5M of deliveries moving from Q2 to Q3

- Stock reaction: +14.7% on May 7 (EUR 41.05 close)

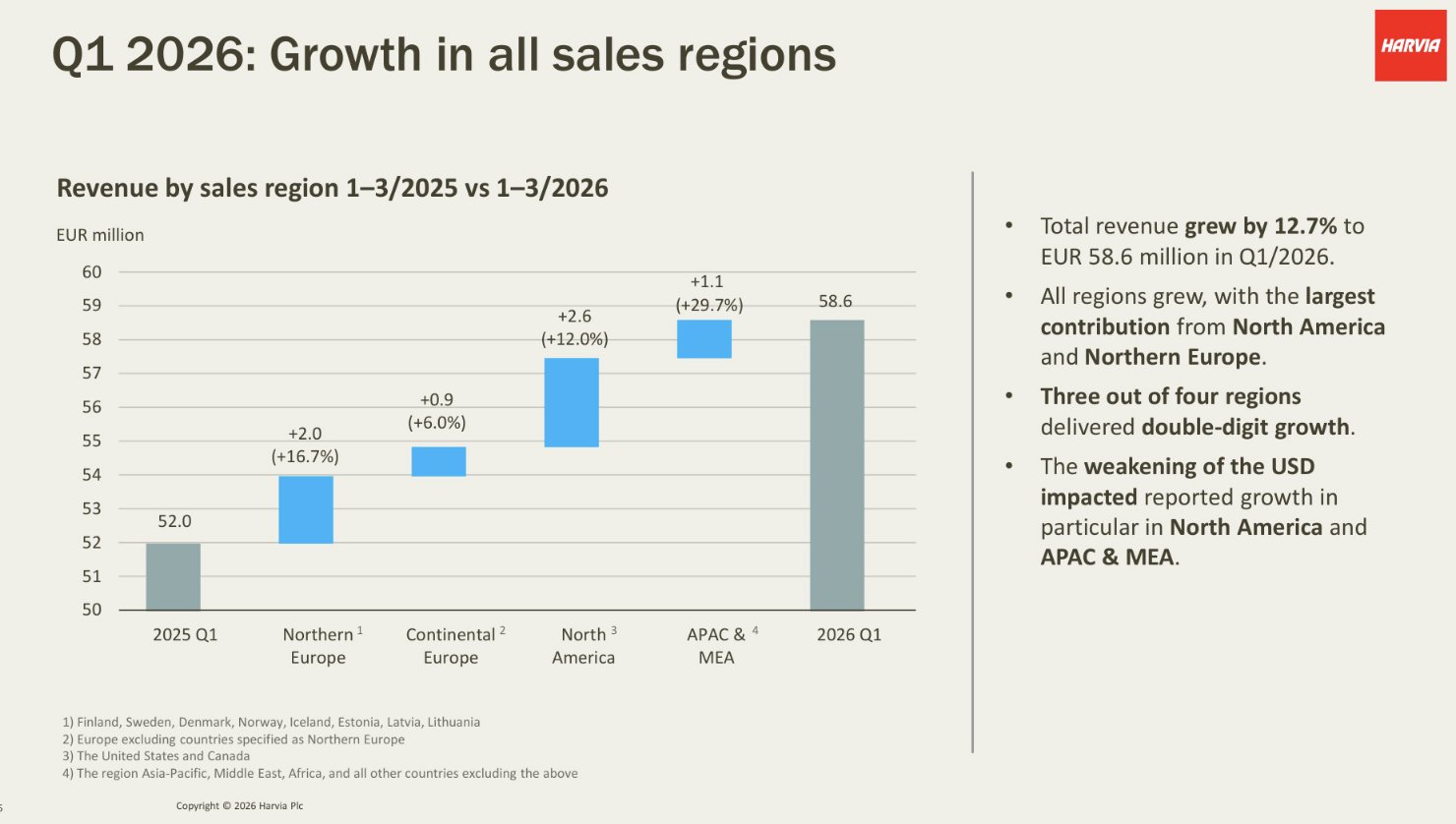

Record Revenue Across Nearly Every Region

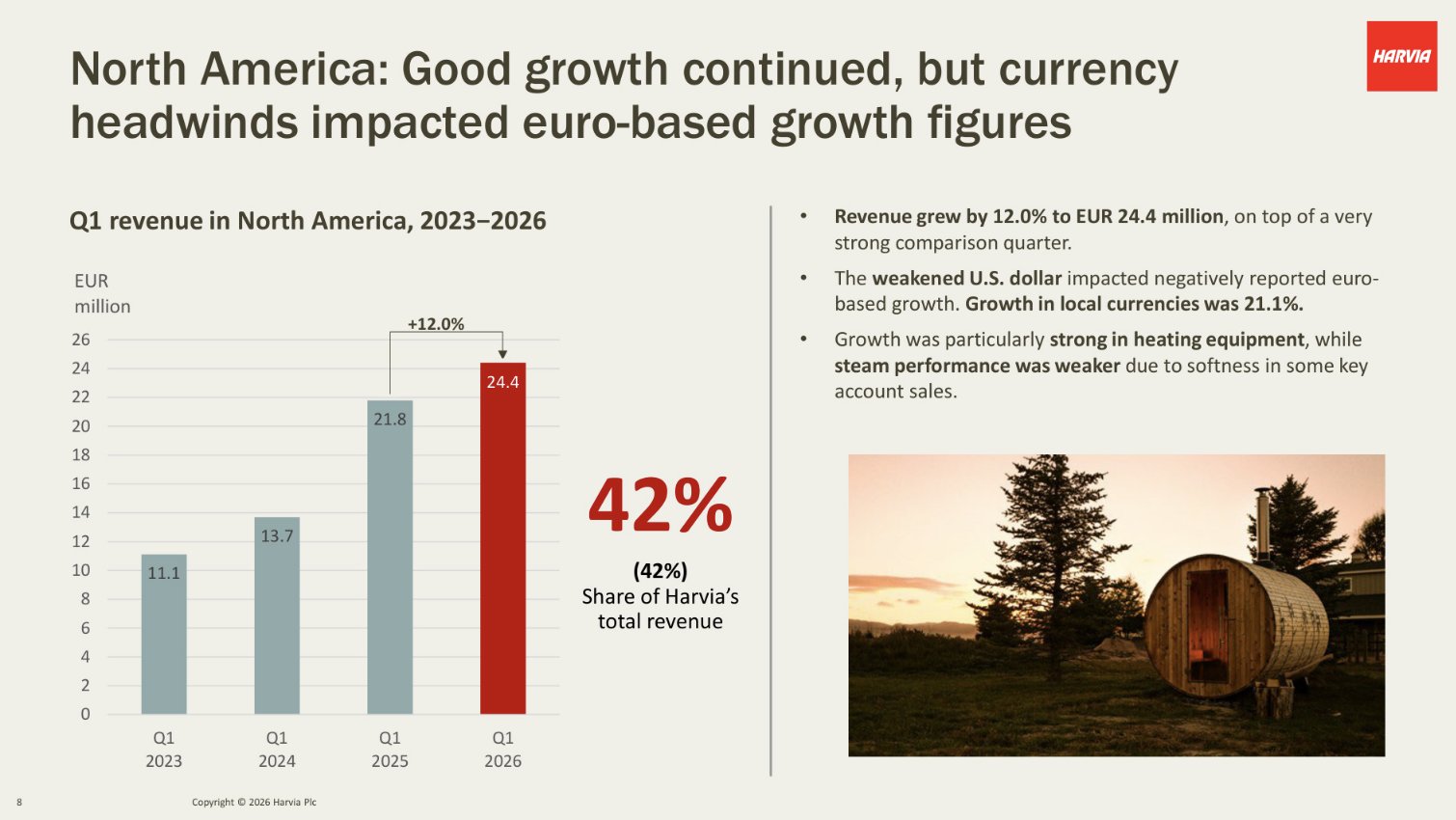

The EUR 58.6 million in Q1 revenue surpassed the previous quarterly record set in Q4 2025 and built on what was already a strong comparison period. North America, the company's largest region at EUR 24.4 million, grew 12% in reported terms and 21.1% in local currencies, stacked on top of 58.8% growth in Q1 2025, when the ThermaSol acquisition was ramping.

"This comes on top of a strong comparison period, as we grew 58.8% in the region in the same quarter last year," CEO Matias Jarnefelt said in the interim report. Growth was driven primarily by heating equipment, while steam products were softer due to weakness in certain key account sales.

Northern Europe posted EUR 13.9 million (+16.7%), its third straight quarter of double-digit gains. Jarnefelt credited systematic distribution expansion in Scandinavia and pent-up demand following slower years, though he noted that the macroeconomic environment "remains subdued." Continental Europe added 6%, steady but unremarkable. APAC and MEA was the standout at +29.7%, powered by China and Japan, with the Gulf region (about 2% of global sales) seeing only limited impact from Middle East instability.

Profitability: The FX Wrinkle

Adjusted operating profit was EUR 12.9 million, an 8.1% increase, with an adjusted margin of 22.0%. That comfortably clears Harvia's long-term target of exceeding 20%. But the gap between 22.0% reported and 22.4% at comparable exchange rates tells a persistent story: the weakening U.S. dollar shaved roughly EUR 0.9 million off operating profit, dragging the margin by about 40 basis points.

For a company that now earns its largest regional revenue in North America, FX translation risk is structural, not incidental. The dollar weakness hit hardest in saunas and Scandinavian hot tubs and in steam products, both categories heavily weighted toward U.S. sales.

Cash generation was strong. Operating free cash flow reached EUR 12.0 million (up from EUR 10.2 million), and cash conversion of 80.5% was well ahead of the 73.7% in Q1 2025. Net debt fell to EUR 49.4 million, putting the net debt-to-EBITDA ratio at 1.0x, less than half the company's 2.5x ceiling.

The Muurame IT Cutover: The Variable to Watch

The number that will shape earnings coverage for the next six months is not in the income statement. It is in the operational guidance: Harvia's ongoing IT infrastructure and process modernization at the Muurame headquarters and factory complex will be completed during Q2, and the cutover is expected to temporarily extend delivery lead times.

Management estimates the disruption will shift approximately EUR 3 to 5 million of deliveries and their associated gross margin from the second quarter into the third. Personnel and indirect costs at Muurame will also rise temporarily during the transition.

"Harvia estimates that no sales will be lost," the company stated in its Q1 presentation. "Benefits will begin to materialize shortly after the upgrade, with meaningful impact already expected in Q3."

The upgrades promise higher automation (including AI-driven capabilities), improved operational resilience, and greater business transparency. For analysts modeling Harvia's quarterly cadence, though, the shift creates a specific optical distortion: Q2 will look compressed, Q3 will look artificially strong, and only the H1 total will give a clean read on underlying momentum. Investors who trade the quarterly print should adjust expectations accordingly.

Balance Sheet Signals M&A Capacity

With EUR 53.4 million in cash and a net debt-to-EBITDA ratio of 1.0x against a 2.5x target ceiling, Harvia's balance sheet carries substantial unused capacity. The company's loans from credit institutions stand at EUR 95.4 million, unchanged from a year earlier, and the equity ratio improved to 49.9% from 47.7%.

Harvia has not made an acquisition since the USD 30.4 million ThermaSol deal in 2024, which added U.S. steam distribution and a production base in Lewisburg, West Virginia. The company's long-term growth target of 10% annual revenue growth historically assumes a mix of organic and inorganic contributions. With the ThermaSol integration now fully absorbed into the organic base and the balance sheet underleveraged, the question is when, not whether, the next deal happens.

Analyst Reaction

The market's read was swift. Nordea raised its price target to EUR 52 from EUR 49 on May 8, reiterating a Buy rating. It was the third consecutive target increase from the bank (EUR 47 to 49 in April, now 49 to 52). Inderes moved the other direction, downgrading to Accumulate from Buy while holding its EUR 44 target, a signal that the 15% stock jump had priced in much of the upside the firm was already modeling. The analyst consensus target sits at EUR 46.

Harvia does not publish short-term guidance. Its long-term financial framework calls for 10% average annual revenue growth, adjusted operating margins above 20%, and net debt below 2.5x adjusted EBITDA. All three targets were met or exceeded in Q1. The EUR 0.77 per share dividend approved at the April AGM will pay its second installment in October.

Why It Matters

Harvia's Q1 is the cleanest set of numbers the sauna industry's largest public company has posted since the post-pandemic normalization began. Revenue is at an all-time high, every region grew, and the organic engine is running without acquisition tailwinds for the first time since ThermaSol closed.

But the Q1 headline will not repeat cleanly in Q2. The Muurame IT cutover creates a EUR 3 to 5 million timing shift that will compress the next quarterly print and inflate the one after it. For operators and suppliers benchmarking against Harvia's demand signals, the H1 total will be more informative than either quarter alone. For investors, the real test is whether the stock's 15% single-day pop holds through what will look, on paper, like a softer Q2. The underlying business is accelerating. The calendar just got rearranged.

Arlene Scott

Senior Wellness Correspondent & Hospitality Consultant

Arlene Scott brings over fifteen years of reporting and consulting experience across energy infrastructure, sustainable design, and thermotherapy-focused hospitality.

Full byline

Arlene Scott is a Senior Wellness Correspondent for SaunaNews.com, bringing over fifteen years of experience at the intersection of energy infrastructure, sustainable design, and thermotherapy. Her work focuses on the physiological benefits of passive heat therapies and the sustainable integration of sauna culture into modern wellness routines.

Arlene's background is rooted in the clean energy transition. She was a founding writer at MicrogridMedia.com, where she covered the technical and economic viability of desalination projects, microgrid deployments, and distributed renewable energy systems. During the mid-2010s, she was a regular contributor to Greentech Media (GTM) during its independent era — prior to the Wood Mackenzie acquisition in 2016 — reporting on the early integration of thermal energy storage and sustainable infrastructure.

Transitioning her focus from macro-energy systems to human-scale wellness, Arlene now applies her technical background to the hospitality sector. She operates as an independent consultant, advising boutique hotels and eco-resorts on the design, energy efficiency, and historical authenticity of commercial sauna and thermal spa installations. Her consulting work ensures that high-end wellness facilities balance traditional Nordic bathing principles with modern sustainable engineering.

Arlene holds a specialized certification in Applied Thermic Wellness from the Nordic Institute of Passive Heat Studies (NIPHS) and is a recognized associate member of the International Sauna Association (ISA). When she isn't reviewing the latest innovations in infrared technology or consulting on a new resort project, Arlene can be found tending to her own traditional wood-fired sauna in the Pacific Northwest. You can read her complete archive of essays on energy, wellness, and sustainable living at www.arlenescott.com.